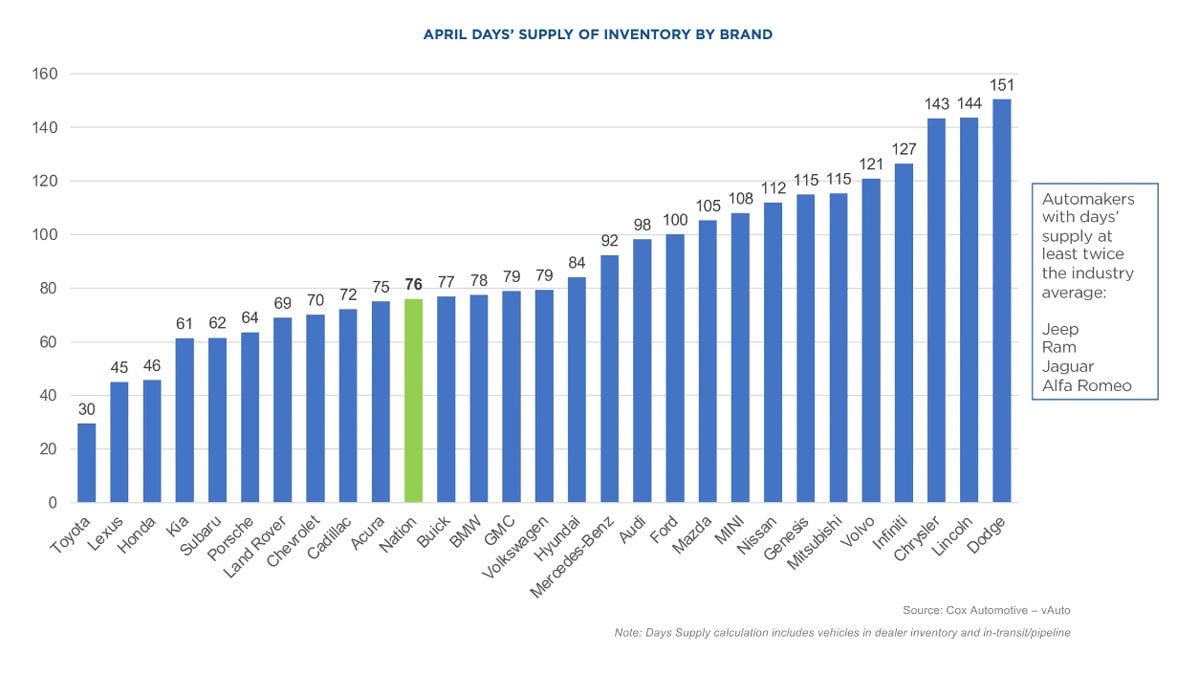

America’s car dealers try to keep about 60 selling days’ worth of cars in stock. They started April with 74, on average. They ended it with 76.

Sixty selling days isn’t a rule, just an old guideline that steers inventory at many dealerships. But there are hard finances behind it.

Unsold Cars Eat Into Dealer Profit

Dealers rarely own the cars on their lots. They’re generally making payments on each one through a complex floating financial arrangement called a floorplan loan. The floorplan cost increases as cars sit unsold and decreases as buyers drive them out the door.

So, an unsold car isn’t just money a dealership hasn’t made yet; it’s a growing expense. The automakers that build cars don’t want that outcome, either, because it stops money flowing to them.

But few dealers keep less than 60 days’ supply, reasoning that they need enough variety in the inventory to showcase combinations of features and colors.

So They Discount Them

When inventory levels floated much over 60, automakers advertise incentives (“get $2,000 cash back!”), and dealers accept lower offers in negotiations, both hoping to get the numbers down.

Pre-pandemic, incentives routinely made up 10% of the average sale. They almost disappeared at the peak of the COVID-19 era. Automakers couldn’t get microchips to build enough cars to get dealers anywhere near 60 days’ supply, so most cars sold at or over sticker price.

But the incentive total has been inching back up ever since. At the end of last quarter it hit 6.6%, according to data from Kelley Blue Book parent Cox Automotive.

The industry briefly worried about that and pulled incentives back a bit as the second quarter started. In April, incentives made up 6.3% of the average deal. The average new car buyer paid $48,510 and got less help from discounts than they would have a month before.

The result? Inventory went up. That’s not good for the dealership or the factory, so we expect to see discounts mount a quick comeback.

Dealers Worried About Shoppers Staying Home

Automakers have a lot to worry about in 2024. Prices aren’t the thing keeping most buyers at home. High interest rates make affording a new car challenging even as prices drop. The Federal Reserve had signaled its intent to cut interest rates several times this year. But, amid stubborn inflation news (partly thanks to soaring car insurance costs), Fed chair Jerome Powell this week warned that any cuts may be further in the future than expected.

So dealers need to move metal, and loan terms won’t improve anytime soon.

Good car deals are the only thing that could work.

Discounts Likely at Some Brands, But Not All

The situation isn’t the same at every sales lot. Toyota, Lexus, and Honda have managed their inventory situation so well that all three remain under 60 days. You won’t talk their dealers into much of a discount. Kia, Subaru, and Porsche are all nearly on target for 60.

But the average brand has 76 days’ supply, and an astonishing 14 brands have over 100. They include luxury marques like Jaguar and Genesis and affordable brands like Mazda and Dodge.

Four companies — Jeep, Ram, Jaguar, and Alfa Romeo — have the dubious honor of carrying more than double the industry’s average inventory.

The bad news? More affordable cars are in short supply. Dealers have more than a 90-day supply of cars priced over $50,000.

The entire industry appears to have miscalculated when it comes to affordable cars. They spent several years adding more high-priced cars to their lineups and canceling production of the cheapest cars. Now, dealers find they lack the affordable cars many buyers want and are pleading with automakers to design more.